Introduction to Funding Societies

The funding societies have grown over the years to become one of the leading alternatives to other conventional banking institutions in terms of business capital and investor portfolio diversification. These platforms signify an overly broad offering of business loans, financing solutions, and investment opportunities in regions such as Singapore compared to conventional financial systems.

Funding societies act like any other online marketplace: businesses in need of loans are matched with individual and institutional investors who fund loans in hopes of earning returns. They offer more flexible and quicker ways for businesses to gain access to funding, while traditional banks often make difficult requirements and have a very lengthy approval process. This is much more helpful to small businesses or startups that are generally barred from accessing credit.

The funding societies ensure a competitive return to investors through investments in business loans or other forms of financing options provided by the platform. Investors are enabled to take part in SME development and, simultaneously, earn attractive yields on investment.

Funding societies have experienced a sudden boom in Singapore due to the conducive regulatory environment, which fosters innovation in financial technologies. Indeed, such platforms have turned out to be the major ones involved in the investment and financing arena, where opportunities are increasingly seen as critical by both businesses and individual investors.

What Are Funding Societies?

Funding societies, in this context, are online platforms matching businesses requiring funding with individual and institutional investors seeking investment avenues. Such a platform offers a new and modern way, in a completely digital environment, of access to business loans-easier for the businesses to access such loans and equally easier for the investors to fund the loans in question in return for returns.

With a generally supportive regulatory environment and an ever-increasing demand for quicker and more flexible financing, the funding societies in Singapore develop very fast. Their primary activity is P2P lending: a mode of raising loans directly from investors, bypassing banks or any other traditional lender.

Funding societies, therefore, provide an alternative source of finance for businesses. This access is usually quicker and less restrictive compared to traditional loans. It also means that businesses can apply for loans with fewer requirements, and most of the time, they will gain access to the funds much sooner.

Through funding societies, investors get the ability to choose from a selection of various loan products, SME loans, invoice financing, even to the subtlety of equity crowdfunding. Returns have the possibility of being attractive, yet risks are also a possibility, and an investor should carefully assess each of these opportunities.

In other words, funding societies create a win-win situation in which businesses efficiently receive a platform to attain business loans, while on the other hand, investors get a new opportunity for investment. Whether you’re in need of capital for your business or are on the lookout for ways to invest in growing companies, funding societies will offer an accessible and innovative solution.

How Funding Societies Work

Funding societies are basically online platforms which match businesses that need funding with investors who seek returns on capital. These platforms ease the way to secure business loans and, for investors, easier avenues of investing in loans than is possible or efficient through mainstream financial institutions. How funding societies work is as follows:

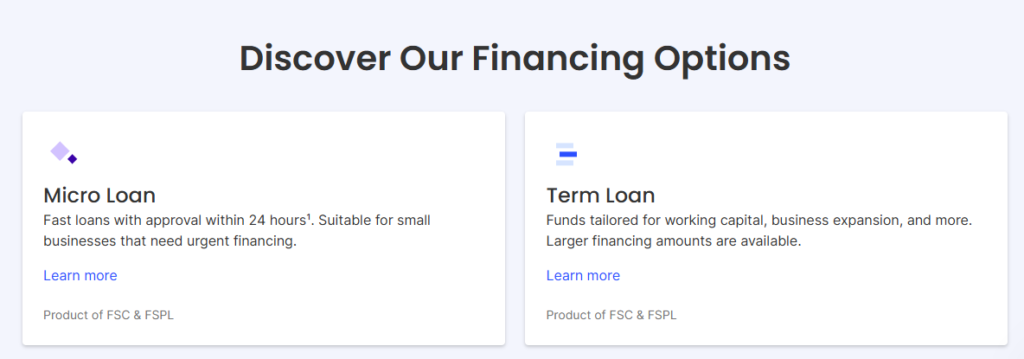

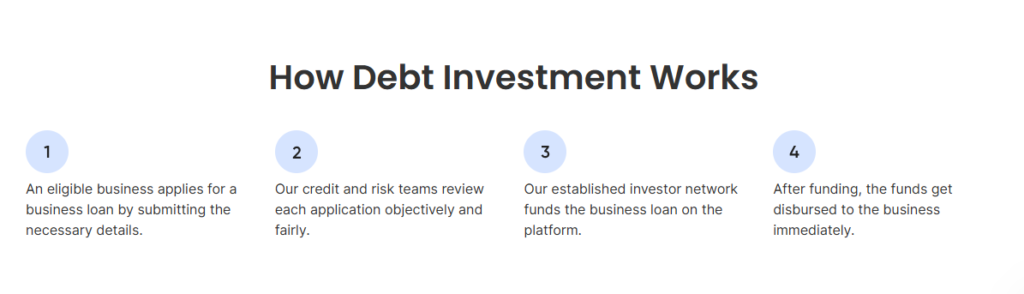

- Application for Business Loans

Businesses requiring finance can apply for the same through a funding society platform. The application, in general, requires information on the business, its financial health, and the purpose of the loan. Depending on the platform, other documents that may be required with respect to the loan request include financial statements or business plans. - Loan Evaluation

Funded societies, on other hand, basically review the loan request of an application made by a business through a mix of automated system and manual reviews. This very step contains assessment about creditworthiness of the business, financial history, and amount of risk in providing the loan. All these factors will in turn be useful in ascertaining the terms of loan, such as rate of interest and payment schedule. - Listing for Investors

The funding society then posts the now-approved loan on its platform for individual and institutional investors to review the details of the loan request. Investors can decide whether they want to fund a part or the entirety of the loan, depending on how much they are willing to invest. - Investing in Loans

Investors peruse various loan offerings on this site and invest in the ones they prefer. Each listed loan normally contains information such as the amount lent, rate of interest, loan period, and profile of the business concerned. A risk-reducing strategy with increased potential returns is where an investor diversifies his investments in funding many types of loans from various businesses. - Disbursement of Funds

The funding society disburses the loan amount to a business once the loan has been fully invested by investors. This way, they gain capital for growth, expansion, or use in operations. - Repayment and Returns

Repayment by the business starts as per the agreed terms, which is usually the payment of installments on a monthly basis. Investors start receiving repayments with interest as per the share they have contributed. Usually, the platform collects and distributes the payments, so no trouble is caused for either of them. - Risk Mitigation

Funding societies may often do something to mitigate the risk for their investors, and examples of such include loan diversification, credit assessment, and at times, guarantees or insurance. However, investors should be very aware of the fact that there is still a certain amount of risk involved in investing in business loans, such as defaults.

The funding societies have recently become so popular in Singapore due to their transparency and ease of use. Another good reason for this is that, through one single platform, a big audience is involved in business loans and investment opportunities. This is a mutual beneficial system whereby businesses access faster financing while investors have opportunities to earn returns on their capital.

Top Funding Societies in the Market

With the emergence of funding societies, businesses have further opportunities to access financing, while investors have been given varied avenues for investment. Some of the leading funding societies in Singapore have emerged at the forefront in facilitating business loans and other forms of funding. Here are some of the top funding societies in the market:

1. Funding Societies Singapore

Funding Societies Singapore is one of the better-known funding societies in Singapore. It matches investors who want to fund business loans with small and medium-sized enterprises in need of access to capital. The platform, through its P2P lending, invoice financing, and SME loans, has facilitated thousands of businesses in securing their much-needed capital. Investors can invest in a range of loan offerings, with typical returns ranging from 6% to 15% per annum, depending on the type of loan and risk profile.

2. MoolahSense

Another key player in the field of lending societies in Singapore is MoolahSense. It offers services such as P2P lending and lends to SMEs, startups, and other businesses. This platform connects the borrowers with individual investors who can facilitate business loans through the platform. MoolahSense provides secured and unsecured loans among various loan products that facilitate quick access to capital for businesses.

3. SeedIn

SeedIn is a leading funding society in Singapore and most of Asia, granting business loans to SMEs. It achieves this by opening up investment opportunities to both retail and institutional investors. On this intuitive platform, businesses can apply for working capital loans, project financing, and invoice financing. SeedIn applies stringent due diligence to loans to ensure only quality businesses make it through; hence, investors enjoy good returns.

4. BondLend

BondLend is a platform specializing in safe businesses loans to SMEs through its P2P lending model. Unique among many others, it deploys a bond-based way of lending whereby businesses receive capital via bond issuance. Investors can purchase the bonds and have the potential of returns as businesses pay back the loan over time. This makes for a safer investment model whereby, usually, the bonds are collateralized by assets or revenue streams of the business.

CapBay

Deal Flexibility Business loans and invoice financing to companies in Singapore and Malaysia. Companies are allowed to raise short-term finance by selling their outstanding invoices to investors on the CapBay platform. This type of financing improves cash flow for companies that might have otherwise had to wait for customers to pay. Investors can finance these different invoice transactions, while returns are then given based on the time of return.

6. CoAssets

CoAssets is the leading funding community that combines P2P lending with equity crowdfunding effectively, thus offering the investors an excellent platform for business loans and investments in equity. Targeting primarily SMEs, CoAssets opens various avenues for businesses to secure loans or equity-based investments, whichever be their requirement. This flexibility in CoAssets attracts both borrowers and investors alike to this platform.

Interest Rates and Fees

When dealing with funding societies for business loans or investment in Singapore, knowledge of the interest rates and fees becomes paramount for both the borrowers and the investors.

Interest Rates for Business Loans

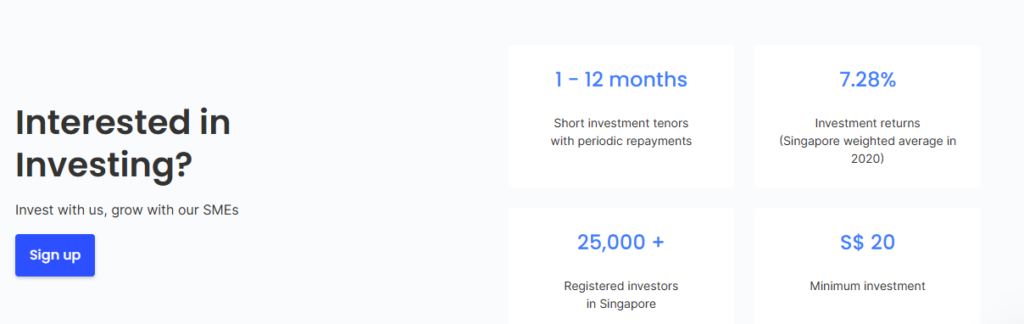

P2P Loans: In general, these range from 6% to 12% per annum, with variations based on the credit risk of the borrower.

Invoice Financing: Generally ranges from 8% to 15%, depending on the size and duration of the invoices.

SME Loans: From 7% to 18%, according to the financial condition of the company.

Investor Returns

Investors may earn 6% to 15% annually, taking into consideration the risk of the loans being invested in. A loan that is higher in its risk can also be potentially higher in returns.

Fees to Borrower

Platform Fee: Usually ranging between 1% and 5% of the amount being borrowed.

Late Payment Fee: In case of delays in payments.

Prepayment Fee: Usually 1% to 3% against prepayment.

Fees Paid by an Investor

Platform Fees: In general, 1% to 2% of returns earned; covers the operational cost.

Loan Terms and Repayment Flexibility

When dealing with funding societies offering business loans and financing, it’s critical to understand its loan terms and repayment flexibility. These two factors will significantly determine the ability of the borrower to pay back and the investor’s returns. Here’s everything you need to know about loan terms and options of repayment in funding societies in Singapore.

Loan Terms

Funding societies actually provide a wide range of grant loan terms for business loans and according to the needs of their borrowers. In fact, usually, the loan term for businesses may range from 6 months up to 5 years. This depends on the size of the loan and also on the platform.

- Short-term Loans: Such a loan usually lasts between 6 and 12 months and is ideal for businesses needing immediate capital, either for working expenses, inventory, or funding towards a project.

- Medium-term loans are usually granted from a period of 1 to 3 years. This loan is provided for expansion or purchase of equipment.

- Long-term Loans: Many platforms give loans that can extend up to 5 years. These are ideal for huge investments, mergers, and acquisitions, or for long-term projects.

Repayment Flexibility

Another advantage related to funding societies involves repayment flexibility for borrowers. Most of the platforms make available different types of repayment schedules in order to handle various cash flow needs of businesses.

- Monthly Installments: It is a very common structure of repayment whereby a business repays the loan in equal monthly installments over the term of the loan. This would definitely help in planning the cash flow more effectively.

- Bullet Repayments: Some loans have the option for a business to make bullet payments, where at the end of term, the full amount is paid. This is ideal if the business is expecting a lump sum of cash at a later date.

- Grace Periods: Most lenders have grace periods for early-stage businesses or those having temporary cash flow problems. In this period, one is not required to pay the complete amount, though interest may be charged.

Most of the funding societies make provisions for early repayments of loans, thereby allowing businesses to clear the loan amount before time and have more flexibility in case they want to reduce their debt burden earlier. Sometimes, there is a prepayment fee that usually ranges from 1% to 3% of the outstanding loan balance.

Early repayment affects the investor’s expected returns through less interest. Some platforms compensate investors, or provide a pro-rated return to investors in cases of early repayment of the loan.

Loan Extensions

Some finance societies may grant extensions of loans or restructuring packages if the business is having trouble repaying. In this case, the business can exercise options to extend the tenures of the loans and lessen the amount that must be repaid monthly. This may involve extra charges or higher interest rates.

Security and Fraud Prevention

When funding societies are used for business loans or investment, security is a primary concern. Here’s how these portals ensure safety:

Data Encryption and Privacy

Funding societies use advanced encryption to protect sensitive data, which is secured in compliance with Singapore’s Personal Data Protection Act (PDPA), making transactions secure and privacy guaranteed for businesses and investors alike.

Credit Risk Assessment

No funding society grants a business loan without first running a detailed credit risk assessment and checking the validity of the business to minimize fraud. This will also include background checks for verification of identity and financial verification.

Secure Payment Gateways

All the transactions made on funding societies are processed through secure payment systems kept safe with SSL encryption; hence, unauthorized access and fraud are prevented.

Fraud Detection and Monitoring

It also employs the use of fraud detection tools, whereby a platform is able to monitor all the transactions made anytime with the help of machine learning for any suspicious activity that may be going on, hence, making it easy to identify fraud in its infancy stage and take precautionary measures against it.

Investor Protection Features

The provision of loan diversification and credit guarantees is very instrumental in bringing down the impact of loses resulting from defaults or fraud. The risk involved is highly minimized, and thus, trust and credibility are gained.

Regulatory Compliance

Funding societies in Singapore are regulated under the Monetary Authority of Singapore to ensure that stern anti-money laundering and know-your-customer standards are upheld.

Investor Returns

Investor returns on funding societies in Singapore range from 6% to 15% per year, depending on the risk level of the loan.

Typical Return Rates

- Low-Risk Loans: from 6% to 8% returns.

- Medium-Risk Loans: from 8% to 12% returns.

- High-Risk Loans: from 12% to 15% returns.

How Returns Are Paid

Returns are normally paid as periodic payments in the form of monthly or quarterly interest. After the term of the loan has elapsed, investors get the principal back along with any remaining interest.

Risk and Returns

Any increase in returns is proportional to an increase in risks. Low-risk loans yield lower returns but are considered very safe, while high-risk loans give higher returns with an increased threat of defaults.

Diversification

Through this diversification across numerous loans with different risk profiles, investors can reduce their exposure to risk and increase returns.

Conclusion

Conclusion Every funding society is an indispensable part of the financial requirements that businesses need to flourish or expand in Singapore. From business loans to investments, no matter what your kind of funding may be, knowing the societies is very important and a key to success in this competitive landscape.

Hence, the funding societies in Singapore offer diversified contact and financial facilities to business entities through flexible options of business loans or investment. To this effect, the societies create windows of opportunity that avail businesses with potential investors or lenders that can address both short-term liquidity and long-term investment strategies.

In fact, as businesses continue to change and innovate, the role of societies in Singapore will only increase in importance. By giving them that opportunity for customized variants of financing, companies can still grow at a comfort level of their choice while giving investors new opportunities to take part in promising ventures Next Blog Post

{kind=link}